Wall Street woke up on March 5, 2026, with a thunderous battle cry that cut through the gloom of a battered SaaS sector: “Buy Snowflake hand over fist.” The stock (SNOW) had cratered 20% year-to-date, trading near $188 after a brutal February sell-off triggered by broader macro fears and AI hype fatigue. Yet top analysts—from Bernstein to Piper Sandler—didn’t flinch. They doubled down, calling the dip a once-in-a-generation entry point for the purest AI Data Cloud play on the market. This wasn’t blind optimism. It was a calculated bet on Snowflake’s unbreakable fundamentals at a time when most AI SaaS names looked expensive and fragile. If you’re hunting for the next 3–5x winner in the “AI SaaS investment” arena, Snowflake stock buy 2026 may be the clearest signal you’ll get all year.

The Bearish Backdrop: 20% YTD Drop Creates a Rare Buying Window

Let’s not sugarcoat it: Snowflake stock has been punished. From its January peak, shares slid 20% amid rising interest-rate worries, slowing enterprise spending, and fears that generative AI adoption would take longer than expected. The March 5 analyst call captured the mood perfectly—headlines screamed “oversold” while the broader Nasdaq SaaS index sat 18% off its highs. Yet this pain is precisely why the bulls are roaring. Valuation has compressed to levels not seen since 2023, while the underlying business has never been stronger. As one Bernstein note put it, “The market is pricing in stagnation; reality is delivering acceleration.” That disconnect is the alpha.

The Unbreakable Moat: Storage-Compute Separation Supercharges AI Scaling

At Snowflake’s core lies the architectural genius that no rival has fully replicated: complete separation of storage and compute. Unlike legacy data warehouses that force you to scale both together (and pay for both), Snowflake lets you spin up or down virtual warehouses in seconds while storage remains infinitely elastic and cheap. In an AI world devouring petabytes for training and inference, this decoupling is pure rocket fuel.

Cortex AI workloads—Snowflake’s native LLM fine-tuning and inference engine—now account for nearly 50% of new compute hours. Customers scale from 1 to 100 warehouses instantly without re-architecture. This elasticity is why Snowflake can handle exabyte-scale AI projects at a fraction of the cost of on-premises or rigid lakehouse alternatives. The result? Explosive usage growth that traditional SaaS metrics simply can’t capture.

Explosive Growth: 30% Q4 Product Revenue Jump Proves AI Demand Is Real

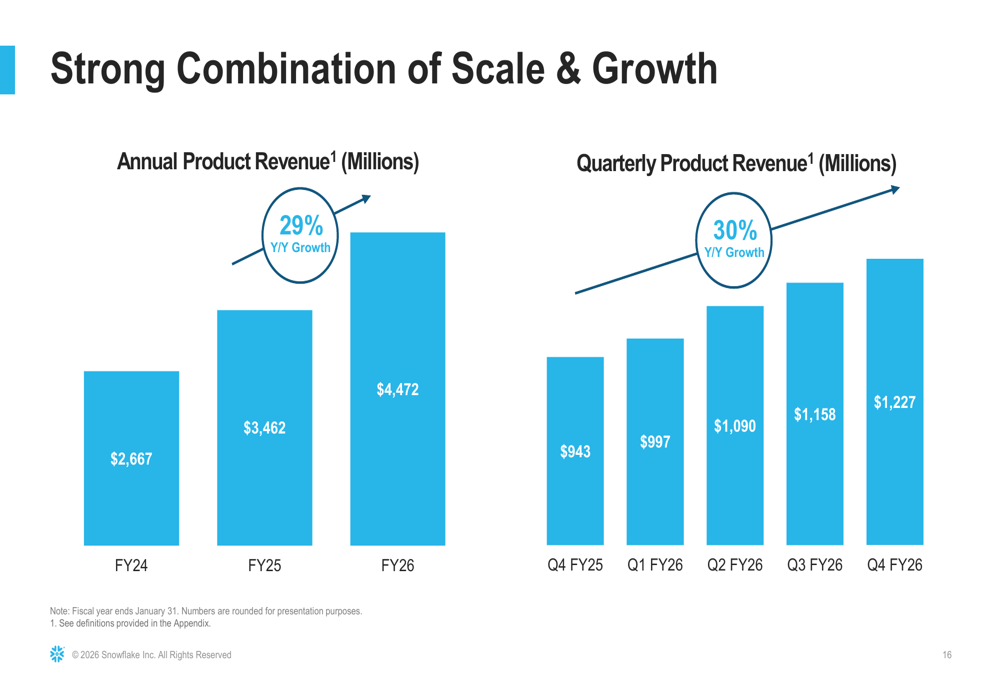

Numbers don’t lie—and Snowflake’s Q4 FY2026 earnings (ended January 31) delivered a masterclass in resilience. Product revenue hit $1.23 billion, up 30% year-over-year, pushing full-year FY2026 to $4.47 billion (+29%). Even more impressive: 733 customers now spend more than $1 million annually (up 27%), and net revenue retention climbed to 125%. These aren’t one-off wins. They’re the direct result of AI workloads exploding inside the platform.

Snowflake Q4 FY2026 slides: 30% revenue growth, margin expansion ahead By Investing.com

Look at the chart above from Snowflake’s official Q4 deck: annual product revenue marching from $2.67B in FY24 to $4.47B in FY26, with quarterly acceleration hitting 30% in Q4. That’s not hype—it’s execution at scale.

Valuation Bargain: 12x Forward P/S Crushes Databricks and Legacy Peers

Here’s where the “buy hand over fist” call gets mathematical. Snowflake trades at roughly 12x forward price-to-sales for FY2027—well below Databricks’ implied 18–20x private valuation and miles cheaper than legacy names like Oracle (still above 15x). The market is paying a discount for Snowflake’s superior growth and margins.

Peer valuation snapshot (March 2026 estimates):

| Company | Forward P/S | FY2026 Revenue Growth | AI Workload % | NRR |

|---|---|---|---|---|

| Snowflake | 12.0x | 29% | ~50% | 125% |

| Databricks | ~18x | 35% (est.) | ~45% | 130% |

| Oracle Cloud | 15.5x | 22% | ~25% | 115% |

| Palantir | 22x | 25% | ~40% | 120% |

Snowflake wins on valuation, multi-cloud neutrality, and proven AI monetization. At 12x, you’re essentially getting the AI upside for free.

Cortex AI Adoption: 200% Surge in Fortune 500 Proves Platform Stickiness

Cortex isn’t a feature—it’s the future. Natural-language querying, custom LLM fine-tuning, and inference endpoints are now live in over 9,100 accounts, with Fortune 500 adoption exploding 200% year-over-year. Enterprises are building proprietary agents directly on their Snowflake data—no data movement, no security headaches, no vendor lock-in.

This adoption wave directly offsets macro risks. While some SaaS peers saw deal slippage in Q4, Snowflake closed multiple nine-figure AI contracts, including the headline $400 million multi-year mega-deal with a global financial institution in February. That single win added hundreds of millions to remaining performance obligations (RPO), which hit a record $9.77 billion (+42% YoY).

Offsetting the Risks: $400M Mega-Deal and Margin Expansion Path

Bears point to high valuation multiples and potential macro slowdown. Bulls counter with ironclad evidence: the $400M deal alone validates enterprise willingness to bet big on Snowflake for AI governance and fraud models. Meanwhile, non-GAAP operating margins expanded to 10% in Q4 and are guided to 12.5% in FY2027. Free-cash-flow margins are tracking toward 23–25%—levels that give Snowflake a war chest to outspend competitors on R&D while still returning capital.

Long-Term Resilience: Why Snowflake Is Built for the AI Decade

The AI spending tsunami is just beginning. Industry forecasts show global enterprise AI investment surging roughly 25–33% annually through 2029, with total spend eclipsing $2 trillion by 2026 and $3.3 trillion by 2029.

State of AI 2026 – AI Market Size, Investment, and Industry Data

This chart from the State of AI 2026 report illustrates the trajectory perfectly. Snowflake sits at the epicenter: every new LLM, agent, or predictive model needs governed, scalable data infrastructure. Competitors are fragmented; Snowflake is the neutral, secure layer that hyperscalers (AWS, Azure, Google) all endorse. That positioning delivers durable 25–30% growth through 2028—exactly what long-term portfolios crave in an “AI SaaS investment” thesis.

Portfolio Strategies: How to Position Snowflake Stock Buy 2026 Today

Smart investors are treating the current dip as a multi-year accumulation opportunity:

- Core Holding (5–10% allocation): Buy on weakness below $190; add on every 5–7% pullback.

- Covered-Call Overlay: Sell out-of-the-money calls against shares to generate 8–12% extra yield while waiting for the rebound.

- Pairs Trade: Long Snowflake / short legacy data names (Oracle, Teradata) to isolate the AI alpha.

- Options Leverage: Use March or June 2026 calls for asymmetric upside if you believe the $250–$300 price targets analysts are quietly modeling.

Risk management is simple: stop-loss 15% below entry, but expect volatility—AI stocks don’t move in straight lines.

Buy or Sell Signals: Clear Roadmap for 2026

Buy triggers:

- Any dip below 11x forward sales

- Cortex adoption metrics exceeding 10,000 accounts

- Next quarterly beat with FY2027 guidance raised above $5.66B

Hold / Add on weakness:

- Current levels (12x P/S with 29% growth)

Sell signals (rare in this bull case):

- Sustained negative NRR or loss of multi-cloud neutrality

Bottom line: The March 5 “buy hand over fist” chorus wasn’t marketing fluff. It was a recognition that Snowflake has transitioned from data warehouse to AI infrastructure titan at the exact moment the market is discounting it most heavily.

If you believe AI spending will surge 25%+ annually—and every credible forecast says it will—then Snowflake stock buy 2026 isn’t a gamble. It’s the highest-conviction AI SaaS investment on the board right now.

Ready to act? Open a position today via your broker, set price alerts below $185, and join the next Snowflake investor webinar for the latest Cortex roadmap. The bearish noise will fade; the AI tailwinds are only getting stronger.