The AI Data Boom: Why Snowflake’s Latest Earnings Matter More Than Ever

In the blistering furnace of the AI revolution, data isn’t just fuel—it’s the entire engine. As enterprises scramble to harness generative AI for everything from predictive analytics to autonomous agents, the demand for scalable, secure data platforms has exploded. Enter Snowflake Inc. (NYSE: SNOW), the AI Data Cloud pioneer that’s become synonymous with breaking down silos and supercharging AI workflows. On December 3, 2025, Snowflake dropped its Q3 FY2026 earnings bomb, revealing a revenue beat amid a sea of AI tailwinds—but also guidance that sent shares tumbling 10% in after-hours trading. Two days later, on December 5, with the stock at $238.65 (down 9.94% intraday), investors are dissecting whether this is a dip to buy or a sign of maturing growth pains.

This isn’t just quarterly numbers; it’s a litmus test for the $100B+ AI data management market projected by 2028 (IDC). Snowflake’s results underscore a pivotal shift: AI isn’t hype anymore—it’s delivering $100M in annual run-rate revenue for the company, with tools like Snowflake Intelligence achieving the “fastest adoption ramp in Snowflake history.” But in a landscape crowded by Databricks’ ML prowess and MongoDB’s NoSQL agility, can Snowflake sustain its 125% net retention rate (NRR) while fending off valuation skeptics? Let’s break it down.

Q3 FY2026 Results: Key Metrics That Beat Expectations

Snowflake’s Q3, ended October 31, 2025, showcased resilient growth in a macro environment still shadowed by economic jitters. Total revenue clocked in at $1.21 billion, a 29% year-over-year (YoY) surge that topped analyst consensus of $1.18 billion. This beat wasn’t a fluke; it reflects deepening enterprise adoption of Snowflake’s multi-cloud architecture, where storage and compute decouple for elastic scaling.

Here’s a bullet-point snapshot of the standout metrics:

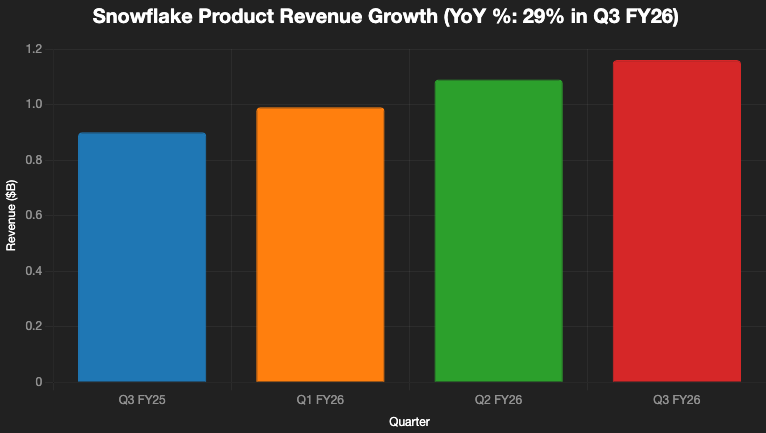

- Product Revenue: $1.16 billion, up 29% YoY—driven by AI workloads and expansions among its 10,000+ customer base. This marks a slight deceleration from Q2’s 32% growth but signals steady momentum.

- Remaining Performance Obligations (RPO): Ballooned to $7.88 billion, a robust 37% YoY increase. Current RPO (upfront commitments) grew even faster at 46%, highlighting multi-year AI contracts locking in future revenue.

- Non-GAAP Operating Margin: Expanded to 11% ($131.3 million income), up from 8% in Q2, as Snowflake tames costs amid R&D investments in agentic AI. This edges closer to the company’s long-term 25% target.

- GAAP EPS: A loss of $(0.87) per share, narrower than the prior year’s $(1.00), though it missed whispers of deeper profitability.

- Net Retention Rate (NRR): Steady at 125%, meaning existing customers ramped spend by 25% on average—fueled by AI upsells like Cortex Analyst for natural language queries.

Guidance for FY2026 was raised modestly: Product revenue now at $4.446 billion (28% YoY growth), with non-GAAP operating margins at 9% and adjusted free cash flow margin at 25%. Q4 product revenue guide of $1.13-$1.14 billion landed in-line, sparking the post-earnings selloff as investors craved more acceleration.

To visualize the revenue trajectory, here’s a bar chart comparing product revenue growth across recent quarters:

This chart illustrates the consistent climb, with Q3’s 29% YoY underscoring AI’s stabilizing force amid a tougher sales cycle.

Historical Context: Building on Q2’s Strong Foundation

To appreciate Q3’s import, rewind to Q2 FY2026 (ended July 31, 2025). That quarter set a high bar with $1.09 billion in product revenue (32% YoY) and the same 125% NRR, plus 654 customers exceeding $1M in trailing-12-month spend—a 27% YoY jump. Snowflake also unveiled AI innovations like Cortex ML Functions, enabling in-platform model training without data movement.

Q3 built on this by sustaining NRR while accelerating RPO—up from Q2’s implied ~$6.5 billion (based on sequential trends). Margins improved sequentially from 8% to 11%, reflecting efficiencies in Snowflake’s consumption-based model. Yet, the EPS miss and in-line guide echo Q2’s post-earnings dip (down 5%), a pattern for high-flyers trading at premiums. CEO Sridhar Ramaswamy noted in the earnings call: “Snowflake is the cornerstone for our customers’ data and AI strategies,” emphasizing partnerships with AI leaders to “supercharge the entire data lifecycle.”

Competitive Landscape: Snowflake vs. Databricks and MongoDB in the AI Arena

Snowflake doesn’t operate in a vacuum. Databricks, the Spark-powered ML darling, and MongoDB, the NoSQL agile beast, are nipping at its heels in the $200B cloud data market.

- Vs. Databricks: Snowflake excels in structured warehousing and ease-of-use (ideal for SQL-savvy analysts), but Databricks dominates ML/ETL with up to 5x faster processing and 12x for big data workloads—albeit at 3.6x higher TCO for ETL. Databricks’ private valuation (~$43B) reflects its AI lakehouse edge, but Snowflake’s multi-cloud neutrality and 99.9% uptime give it a governance moat. In Q3, Snowflake’s AI run rate hit $100M, closing the gap on Databricks’ MosaicML integrations.

- Vs. MongoDB: While Snowflake handles petabyte-scale analytics, MongoDB shines in flexible, document-based apps for real-time personalization. Both leverage vector search for RAG (retrieval-augmented generation), but Snowflake’s structured data fabric complements MongoDB’s NoSQL—leading to 35% YoY joint deployments. MongoDB’s Q3 (Dec 2) beat with 19% growth pales vs. Snowflake’s 29%, but its dev-focused ecosystem keeps it nimble.

Per Gartner Peer Insights 2025, Snowflake leads in cloud DBMS with 4.5/5 ratings for scalability, outpacing Databricks (4.3) in enterprise adoption but trailing in ML innovation. Snowflake’s play? Embed AI natively, like Cortex’s LLM toolkit, to blur lines with rivals.

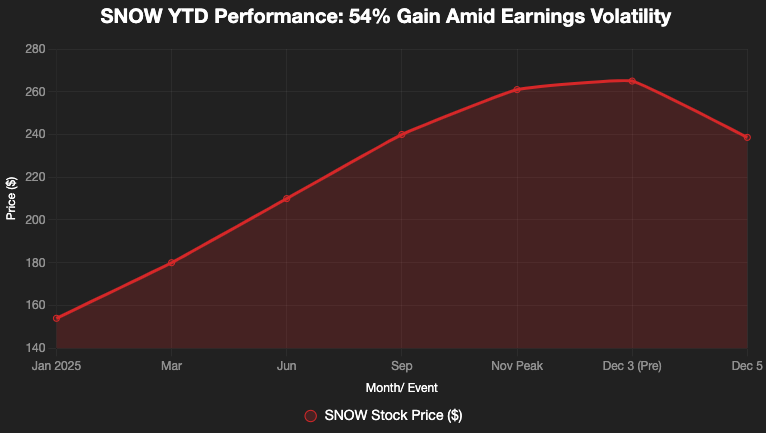

Stock Performance: From 63% YTD Rally to Post-Earnings Reality Check

Snowflake’s shares rocketed 63% YTD through November, outpacing the S&P 500’s 25% on AI euphoria—peaking near $261. But Q3’s in-line guide triggered a 9.97% plunge to ~$215 on Dec 4, settling at $238.65 by Dec 5 (YTD +54.56%). Trading at 13x forward sales (down from 15x), it’s “rich” but backed by 120%+ NRR and $7.88B RPO visibility.

Analysts remain bullish: Post-earnings, Morgan Stanley hiked its target to $299 (Overweight), and consensus sits at $281 (up 18% from current). Bull case: AI beats drive 30%+ growth; bear: Macro headwinds cap margins at 9%.

Here’s a line chart tracking SNOW’s YTD stock performance:

Volatility is the price of AI leadership—expect more as agentic AI ramps.

Investor Scenarios: Bulls Charge, Bears Circle

- Bullish Beat: If Q4 exceeds on AI (e.g., Cortex in 25%+ accounts), shares rebound to $300+ by FY-end, validating 28% growth as conservative. Partnerships like NVIDIA CUDA-X could add 10x ML speed, per Q3 call.

- Valuation Risks: At 13x sales, any macro slowdown (e.g., delayed AI ROI) could drag to $200. Competition intensifies if Databricks IPOs at 20x multiples.

Per Piper Sandler (Dec 4), “Buy the dip—AI is Snowflake’s moat.”

Actionable Advice for Data Professionals: Leverage the Momentum

For data engineers and analysts, Q3 screams opportunity. Prioritize Cortex for zero-ETL AI pipelines—reducing prep time by 40% (Gartner). Migrate to Snowflake Intelligence for agentic querying, especially if you’re on legacy warehouses. Budget for multi-cloud: Its 99.9% SLA beats single-vendor lock-in.

Start small: Pilot RPO-backed expansions with $1M+ spend thresholds for discounts. Track NRR in your org—aim for 120% via AI upsells. In a Databricks-heavy shop? Hybridize with Snowflake’s Iceberg support for seamless federation.

Tune In: What’s Next for Snowflake’s AI Odyssey?

Snowflake’s Q3 FY2026 isn’t flawless, but it’s proof-positive of AI’s transformative pull—$100M run rate and 37% RPO growth amid headwinds. As Ramaswamy eyes a “unified AI Data Cloud,” the stage is set for 2026 dominance.