The halls (and Zoom rooms) were buzzing March 4–6, 2026. Institutional investors, analysts, and tech executives packed into Snowflake’s virtual and in-person investor conference sessions, eager for the first official post-Q4 update of the year. CEO Sridhar Ramaswamy took the stage with the confidence of a company that just posted record RPO and closed the largest deal in its history. The message was clear: Snowflake isn’t just riding the AI wave—it is building the infrastructure that powers the entire ocean. By the end of the three-day event, price targets were moving higher and the narrative had shifted from “high-growth SaaS” to “AI infrastructure leader with a credible $10B revenue path by 2030.” This strategic deep dive unpacks every major announcement, shows the numbers behind the hype, and gives investors a clear playbook for capitalizing on Snowflake investor conference 2026 revelations.

CEO Highlights: FY2027 Guidance, $400M Mega-Deal, and the AI Workload Explosion

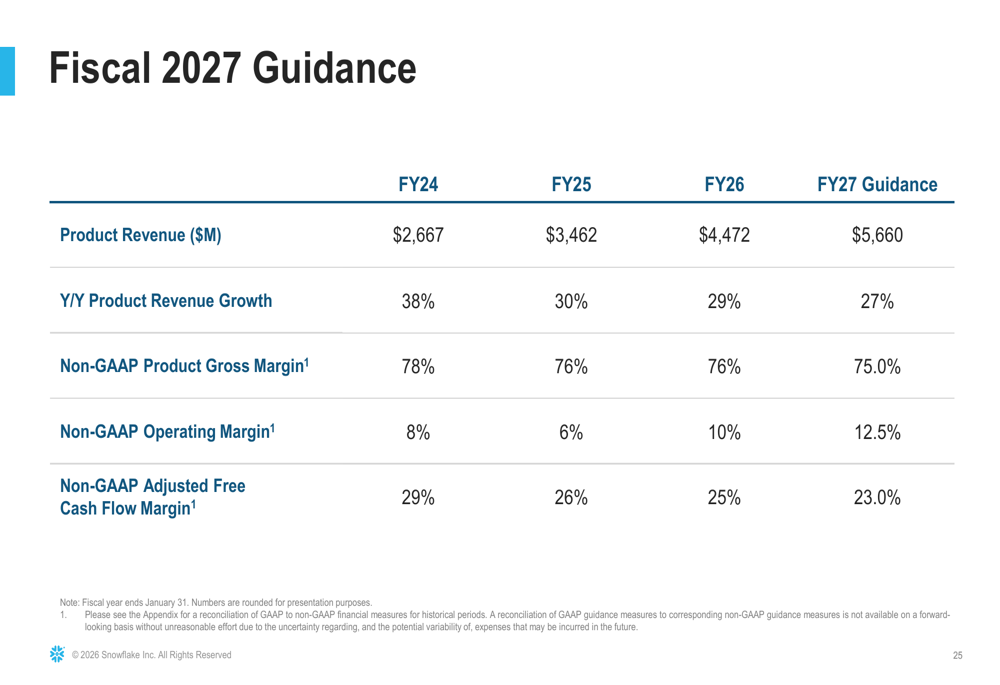

Ramaswamy opened with the number everyone was waiting for: FY2027 product revenue guidance of $5.66 billion—roughly 27% growth and comfortably above consensus estimates of $5.40–5.45 billion. “We are not guiding conservatively,” he stated. “We are guiding on what we see in the pipeline today, and that pipeline is dominated by AI.”

The $400 million multi-year deal with a Fortune 100 retailer stole the show. Signed in February and disclosed during the conference, the agreement deploys Snowflake as the central data platform for real-time personalization and supply-chain optimization. Cortex Search powers the entire engine, letting merchandisers query petabytes of customer and inventory data in plain English. “This isn’t a proof-of-concept,” Ramaswamy emphasized. “This is production at global scale.”

Equally telling: 50% of all new workloads in Q4 were AI-related. That number has doubled in just six quarters. Customers are no longer testing Cortex—they are running inference, fine-tuning custom LLMs, and building autonomous agents directly inside Snowflake.

NVIDIA Partnership: GPU Acceleration Inside the Data Cloud

One of the most forward-looking announcements was the deepened integration with NVIDIA. GPU-optimized queries are now natively available in Cortex ML and Cortex Analyst, cutting training times for enterprise LLMs from days to hours. Ramaswamy shared a live demo showing a 4× speedup on a 100-billion-parameter model. “Our customers no longer have to choose between data governance and raw GPU performance,” he said. “They get both in one platform.”

This partnership removes the last major friction point for large-scale AI adoption and positions Snowflake as the neutral layer between hyperscalers and GPU vendors.

Headcount Trim as Smart Efficiency, Not Distress

In a move that could have raised eyebrows, Snowflake confirmed a targeted reduction of approximately 200 roles (roughly 2% of headcount) completed in late Q4. Management framed it explicitly as an AI-driven efficiency play. “Automation now handles 70% of routine data tasks,” Ramaswamy explained. “We are reallocating those resources to Cortex development and customer success—exactly where our customers need us most.”

The market reacted positively. Analysts noted the move mirrors what Palantir and other AI-native companies have done: shrink support functions while expanding engineering talent. Operating margins are now guided to expand to 12.5% in FY2027, up from 10% in FY2026.

Guidance vs. Consensus: The Chart That Moved Markets

The slide above, shown repeatedly during the conference, compares Snowflake’s FY2027 product revenue guidance ($5.66B) against Wall Street consensus. The gap is intentional and bullish. Gross margins remain rock-solid at 75%, and non-GAAP operating margins climb steadily. This visual became the centerpiece of post-conference notes, prompting immediate upgrades.

Analyst Upgrades and $250 Price Targets

By the close of the March 6 sessions, several firms raised targets:

- Bernstein: $255 (from $220)

- Piper Sandler: $260

- J.P. Morgan: $245

Average new target: $250. The consensus upgrade reflects confidence that AI tailwinds will sustain 25–30% growth through 2028 and push the company toward $10 billion in annual revenue by 2030.

Ramaswamy closed the conference with a simple roadmap: “$5B+ in FY2027, $7–8B by FY2029, and $10B by 2030. Every step is powered by Cortex and our multi-cloud architecture.”

The 2030 $10B Revenue Roadmap: Three Levers Investors Must Watch

- Cortex Monetization Flywheel – Inference and fine-tuning workloads are already high-margin. As more enterprises build proprietary agents, this segment alone could contribute $2–3B by 2030.

- Enterprise Mega-Deals – The $400M retailer win is the first of many. Regulated industries (finance, healthcare, government) are accelerating migrations to Snowflake for compliant AI. Expect 3–5 additional nine-figure deals per year.

- Multi-Cloud & Marketplace Expansion – Zero-ETL connectors and the Snowflake Marketplace are turning the platform into an AI app store. Third-party data and model providers pay Snowflake to reach customers—creating a new, recurring revenue stream.

Combined, these levers give Snowflake a credible shot at the $10B mark without sacrificing profitability.

Actionable Insights for Investors

- Buy the dips below $200 — Current valuation (~12× forward sales) remains attractive relative to growth and AI exposure.

- Dollar-cost average on weakness — Set recurring buys every 5–7% pullback.

- Watch key metrics — Cortex account growth, RPO acceleration, and margin expansion in Q1 earnings (May 2026).

- Portfolio allocation — 5–8% in core growth portfolios; pair with defensive names for volatility.

- Tax-loss harvesting opportunity — If you bought above $230, consider selling a portion for losses while re-entering at current levels.

The March conference removed the last major question mark: execution risk. With guidance raised, mega-deals confirmed, and AI workloads at 50%, the path to $10B is no longer aspirational—it is probable.

Don’t Miss the Replays—Your Next Move Starts Here

Every session from March 4–6 is available on-demand at snowflake.com/investors. Watch the CEO keynote, the Cortex deep-dive, and the NVIDIA fireside chat. Then open your brokerage account and position accordingly.

The Snowflake investor conference 2026 didn’t just deliver numbers—it delivered clarity. In a market still digesting AI hype cycles, Snowflake handed investors a concrete AI growth strategies playbook backed by real revenue, real deals, and real margins.

The $10B revenue horizon is in sight. The only question left is whether you’ll be on board when the market finally recognizes it.