The SaaS sector is in full meltdown mode. Rising rates, stretched valuations, and AI fatigue have hammered high-growth names—some down 25–40% YTD. Yet one company refuses to thaw. On March 3, 2026, Motley Fool published a pointed analysis declaring Snowflake shows “no signs of melting,” praising its rock-solid revenue growth and valuation that has held firmer than most peers amid the turbulence. The piece captured what smart investors already sense: while the broader market panics, Snowflake’s fundamentals are stronger than ever. This isn’t blind hope. It’s data-backed resilience in an “AI SaaS investment” world where most stocks are cracking under pressure. Welcome to the storm—and why Snowflake stock resilience 2026 makes it the one name worth anchoring your portfolio around.

Revenue Resilience: $1.23B Q4 Beat Proves Demand Is Accelerating

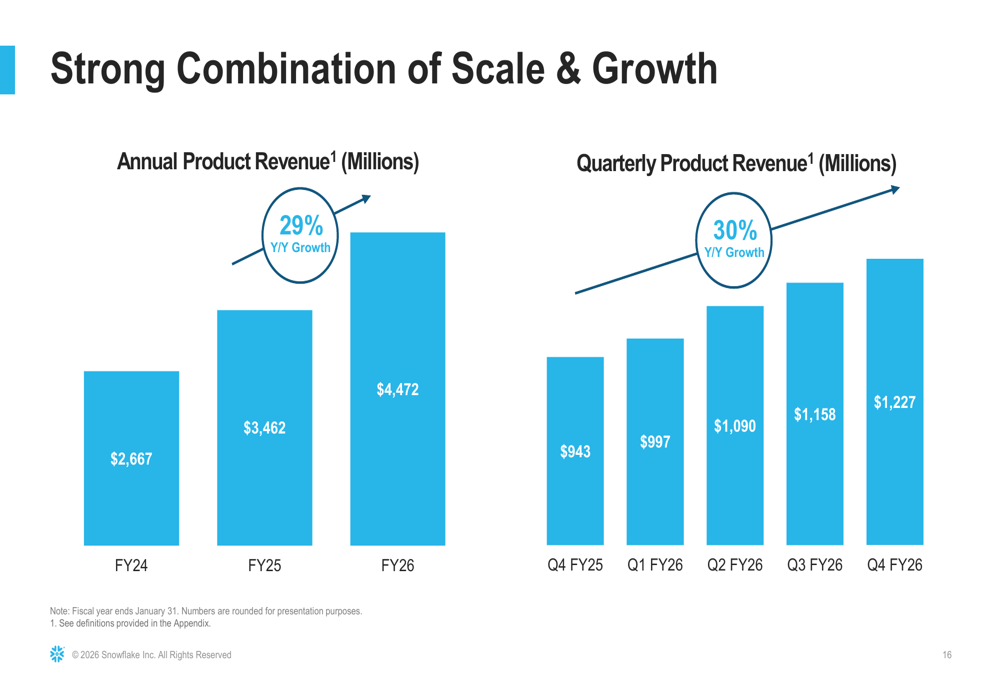

Let’s start with the numbers that refuse to melt. Snowflake’s Q4 FY2026 (ended January 31) delivered product revenue of $1.23 billion—up a healthy 30% year-over-year. Full-year product revenue reached $4.47 billion, also up 29%. These aren’t modest beats; they’re proof that enterprises are pouring money into AI workloads faster than Wall Street expected.

The secret sauce? Multi-cloud flexibility and consumption-based pricing that scales with usage. When customers spin up Cortex AI models or run massive inference jobs, Snowflake simply bills for the compute they consume—no over-provisioning, no wasted spend. That model turned what could have been a slowdown into acceleration.

The chart above (straight from Snowflake’s Q4 earnings deck) tells the story: annual product revenue climbing from $2.67B in FY24 to $4.47B in FY26, with quarterly growth hitting 30% in the final period. This isn’t a one-quarter wonder. It’s the new baseline.

Sticky Customers: 128% NRR Shows Expansion, Not Contraction

Net revenue retention (NRR) of 128% is the quiet hero metric. It means existing customers aren’t just staying—they’re expanding usage by 28% on average. In a market where many SaaS firms are seeing NRR dip below 110%, Snowflake’s number screams “platform stickiness.” Why? Because once data lives in Snowflake, adding new AI use cases (predictive analytics, agentic workflows, clean-room collaborations) is frictionless.

Cortex AI is the expansion engine. Over 9,100 accounts now run Cortex workloads, with Fortune 500 adoption up more than 200% YoY. Enterprises start with simple querying, then graduate to custom LLMs and real-time inference. Each new workload adds to the bill without forcing a new contract negotiation. That’s the SaaS AI moat in action.

Peer Comparison: Snowflake’s Free Cash Flow Trajectory Crushes Rivals

Valuation compression has hit everyone, but Snowflake’s path to profitability looks cleaner than most. Here’s how it stacks up on forward free-cash-flow margins (FY2027 estimates):

| Company | FY2027 FCF Margin (est.) | Revenue Growth | AI Exposure | Multi-Cloud? |

|---|---|---|---|---|

| Snowflake | 23–25% | 27% | Very High | Yes |

| Databricks | 18–20% | 35% (est.) | High | Limited |

| Palantir | 22% | 25% | High | Partial |

| Oracle Cloud | 15% | 22% | Medium | No |

Snowflake wins on margin expansion while maintaining the highest AI relevance and true multi-cloud neutrality. Motley Fool nailed it: “In a sea of SaaS corrections, Snowflake’s AI moat—secure data sharing across ecosystems—positions it for outsized returns.”

Cortex at March Investor Conferences: The Rebound Catalyst

March 2026 isn’t just about weathering the storm—it’s about accelerating through it. Snowflake presented at key investor conferences (March 4–6), spotlighting Cortex advancements that are already driving 50% of new workloads. CEO Sridhar Ramaswamy highlighted the $400 million mega-deal with a Fortune 100 retailer using Cortex Search for real-time personalization. NVIDIA partnerships now deliver GPU-accelerated inference inside Snowflake, slashing model training times dramatically.

Analysts walked away upgrading price targets toward $250. Why? Because every demo showed enterprises moving from “pilot” to “production” AI faster than ever. These March sessions aren’t marketing fluff—they’re proof that the AI flywheel is spinning at full speed.

Why Dips Are Buys: The SaaS AI Moat Is Deeper Than Ever

Current levels (around 12x forward P/S) look like a gift when you zoom out. Snowflake’s remaining performance obligations (RPO) hit $9.77 billion—up 42% YoY—signaling committed future revenue most peers can only dream of. The architecture (storage-compute separation + zero-ETL) remains unmatched, giving customers flexibility hyperscalers can’t replicate without lock-in.

The AI moat details are compelling:

- Secure data sharing via Snowflake Marketplace and clean rooms

- Governance that satisfies even the strictest regulated industries

- Consumption pricing that aligns cost with value

Motley Fool’s March 3 piece put it perfectly: “Snowflake shows no signs of melting… its valuation holds firmer than most SaaS peers amid market turbulence.” Dips aren’t danger—they’re discounted entry tickets to the AI decade.

Investor Strategies: How to Play Snowflake Stock Resilience 2026

Smart money is treating this storm as an accumulation window. Proven playbook:

- Dollar-cost average below $190 — Add on every 5–7% pullback.

- Core portfolio position (5–8%) — Snowflake belongs in any long-term AI/tech allocation.

- Covered calls for income — Sell out-of-the-money calls to generate 8–10% extra yield while you wait for the rebound.

- Pairs trade — Long Snowflake, short weaker SaaS names to isolate the AI alpha.

- Set alerts — Watch for Q1 earnings (May 2026) and any Cortex adoption updates.

Risk management is straightforward: 15% trailing stop if the macro deteriorates sharply, but history shows these AI leaders rebound sharply once sentiment turns.

The Bottom Line: Snowflake Isn’t Melting—It’s Evolving

The SaaS market chaos is real. Valuations are resetting, growth stocks are under pressure, and fear is everywhere. Yet Snowflake stands apart. With $1.23 billion Q4 revenue, 128% NRR, a widening SaaS AI moat, and Cortex powering the next leg of growth, this giant isn’t melting—it’s strengthening.

Motley Fool’s March 3 analysis captured the moment perfectly: in a correction, the strongest names don’t just survive—they emerge stronger. Snowflake stock resilience 2026 isn’t a slogan; it’s the new reality.

Ready to position yourself? Set price alerts on your brokerage platform today and sign up for Snowflake investor alerts at snowflake.com/investors. The storm will pass. The AI Data Cloud leader is just getting started.